The Rise of Robo-Advisors: Comparing Performance and Fees in 2026

Anúncios

The Rise of Robo-Advisors: Comparing Performance and Fees for 5 Top Platforms in 2026 highlights the latest developments in automated investing across the United States.

Based on new details from industry analysts and financial publications, this straightforward update prioritizes what changed, why it matters, and what to watch next in the evolving wealth management landscape.

Understanding the Robo-Advisor Revolution in 2026

The financial world has witnessed a significant transformation with the advent and expansion of robo-advisors.

Anúncios

These automated platforms leverage algorithms to manage investments, offering accessible and often lower-cost alternatives to traditional financial advisors.

As we navigate 2026, the competitive landscape has matured, with platforms continually refining their offerings, from sophisticated AI-driven portfolio rebalancing to personalized financial planning tools.

Investors are increasingly turning to robo-advisors for their efficiency and transparency, making a detailed comparison of performance and fees more crucial than ever.

Anúncios

Key Factors Driving Robo-Advisor Adoption

Several underlying trends are accelerating the adoption of robo-advisors, particularly among younger demographics and those seeking cost-effective investment solutions.

The ease of setting up an account and the automated nature of portfolio management appeal to a broad spectrum of investors.

Technological advancements, including enhanced AI and machine learning capabilities, allow these platforms to offer more sophisticated investment strategies previously exclusive to high-net-worth individuals.

This democratization of advanced financial tools is a significant driver of growth.

Furthermore, the persistent focus on fee transparency and lower costs compared to human advisors remains a compelling argument for many, directly influencing the continued Robo-Advisors Performance Fees discussion.

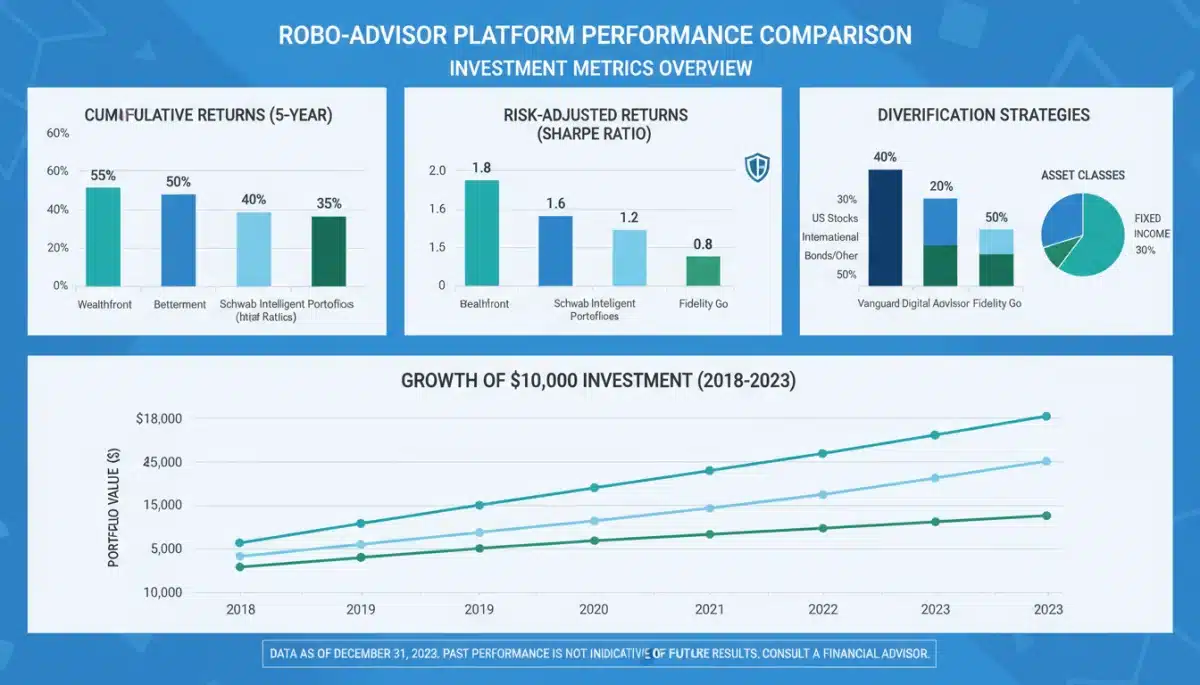

Deconstructing Performance Metrics of Leading Platforms

Evaluating the performance of robo-advisors goes beyond simple returns; it involves understanding risk-adjusted performance, diversification benefits, and how platforms navigate different market conditions.

Each platform employs proprietary algorithms and investment philosophies that dictate their portfolio construction and rebalancing.

For investors, consistent long-term performance, coupled with effective risk management, is paramount. We analyze how top platforms have fared across various market cycles, providing a clearer picture of their resilience and growth potential.

Careful scrutiny of historical data, though not indicative of future results, offers valuable insights into a robo-advisor’s strategic effectiveness and its ability to meet client objectives.

Analyzing Risk-Adjusted Returns

- Sharpe Ratio: This metric assesses return per unit of risk, with higher ratios indicating better risk-adjusted performance. Top robo-advisors consistently aim for optimized Sharpe Ratios.

- Standard Deviation: Measures portfolio volatility; lower standard deviation suggests a more stable investment experience. Platforms often highlight their ability to minimize this.

- Maximum Drawdown: Represents the largest peak-to-trough decline in a portfolio, crucial for understanding potential losses during adverse market conditions.

Diversification Strategies

Effective diversification is a cornerstone of sound investment, and robo-advisors excel in implementing this principle across various asset classes.

They typically invest in low-cost ETFs and mutual funds that span equities, fixed income, real estate, and sometimes even alternative investments.

The automated rebalancing feature ensures that portfolios maintain their target asset allocation, preventing overexposure to certain sectors or asset types. This systematic approach helps mitigate risk and capture market opportunities.

Understanding these diversification strategies is key when comparing Robo-Advisors Performance Fees, as a well-diversified portfolio can significantly impact long-term returns and stability.

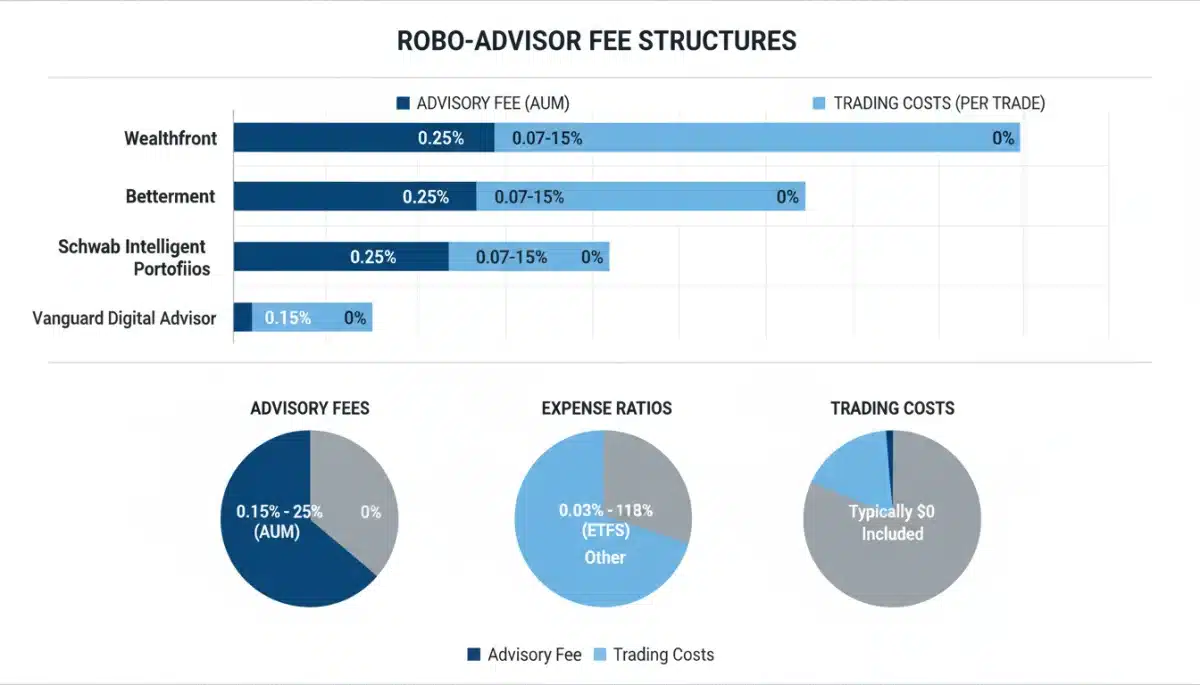

A Deep Dive into Fee Structures: What Investors Pay

Fees are a critical component of any investment decision, directly impacting net returns over time. Robo-advisors generally boast lower fees than traditional financial advisors, but their structures can still vary significantly among platforms.

Typically, fees include an advisory fee, which is a percentage of assets under management (AUM), and underlying expense ratios of the ETFs or mutual funds held within the portfolio.

Some platforms may also charge for specific services or premium features.

Transparency in fee disclosure is a hallmark of leading robo-advisors, allowing investors to clearly understand their total cost of ownership, a vital aspect of the Robo-Advisors Performance Fees equation.

Advisory Fees vs. Expense Ratios

- Advisory Fees: Usually range from 0.15% to 0.50% of AUM annually, paid directly to the robo-advisor for managing the portfolio.

- Expense Ratios: These are embedded costs of the underlying ETFs and mutual funds, typically ranging from 0.05% to 0.25% annually. These are not paid directly but reduce the fund’s returns.

- Trading Costs: While many platforms offer commission-free trading, some specialized funds or services might incur minimal transaction fees.

Impact of Fees on Long-Term Returns

Even seemingly small differences in fees can have a substantial impact on overall investment growth due to the power of compounding. Over decades, higher fees can erode a significant portion of potential returns.

Investors should calculate the total annual cost by combining advisory fees and estimated expense ratios. This comprehensive view allows for a more accurate comparison of the financial impact across different platforms.

Selecting a robo-advisor with a competitive fee structure that aligns with investment goals is crucial for maximizing long-term wealth accumulation, directly addressing concerns about Robo-Advisors Performance Fees.

Top 5 Robo-Advisor Platforms in 2026: An In-Depth Look

In 2026, the market for robo-advisors is dominated by several key players, each offering distinct features, investment methodologies, and fee structures. Understanding these differences is essential for investors seeking the best fit for their financial objectives.

We delve into the specifics of five leading platforms, examining their core offerings, target audiences, and how their performance and fees stack up against each other.

This comparative analysis provides a clear picture of the current competitive landscape in the automated investment sector.

Platform 1: Vanguard Digital Advisor

Vanguard Digital Advisor stands out for its low-cost approach and strong alignment with Vanguard’s reputation for investor-friendly products.

It offers personalized financial plans and automated portfolio management using Vanguard’s renowned ETFs.

Its target audience typically includes cost-conscious investors who appreciate a straightforward, diversified approach. The platform’s fee structure is highly competitive, reinforcing Vanguard’s commitment to minimizing investor costs.

Performance is generally strong, reflecting its disciplined indexing strategy, making it a strong contender in the Robo-Advisors Performance Fees discussion.

Platform 2: Betterment

Betterment pioneered many features now standard in the robo-advisor space, including tax-loss harvesting and goal-based investing. It offers a sophisticated platform with a range of portfolios tailored to individual risk tolerances and financial goals.

The platform appeals to a broad audience, from beginners to more experienced investors seeking advanced optimization features. Its fees are competitive, with options for different service tiers.

Betterment’s performance has been robust, often cited for its intelligent tax strategies that can significantly enhance after-tax returns.

Platform 3: Wealthfront

Wealthfront is known for its innovative financial planning tools, including its “Path” feature, which projects future financial outcomes based on current inputs. It focuses on sophisticated tax optimization and a wide range of investment options.

This platform typically attracts tech-savvy investors looking for comprehensive financial planning alongside automated investing. Its fee structure is transparent and generally aligned with industry averages.

Wealthfront’s performance is often lauded for its ability to deliver strong returns while leveraging advanced tax strategies for maximum efficiency, contributing positively to its Robo-Advisors Performance Fees profile.

Platform 4: Schwab Intelligent Portfolios

Schwab Intelligent Portfolios offers commission-free automated investing, a significant draw for many investors. It provides diversified portfolios built from Schwab ETFs and cash, with rebalancing and tax-loss harvesting.

It caters to investors who prefer a zero-advisory-fee model, although it maintains a cash allocation that might slightly impact overall returns. The platform benefits from Schwab’s extensive resources and strong brand recognition.

Its performance is solid, particularly for those seeking a no-advisory-fee option, making it an attractive choice for many considering Robo-Advisors Performance Fees.

Platform 5: Fidelity Go

Fidelity Go combines automated investing with access to Fidelity’s extensive research and customer support. It offers diversified portfolios managed by Fidelity professionals, with no advisory fees for balances under a certain threshold.

This platform is ideal for investors who value a hybrid approach, blending automation with the backing of a traditional financial giant. Its tiered fee structure makes it accessible to a wide range of investors.

Fidelity Go’s performance is competitive, leveraging Fidelity’s expertise in fund selection and portfolio management.

Comparative Analysis: Performance and Fees Matrix

A direct comparison of performance and fees reveals the nuances that differentiate these top robo-advisors. While all aim to provide efficient, low-cost investing, their approaches to achieving these goals vary.

Performance metrics, including annualized returns and risk-adjusted figures, must be viewed in conjunction with the total cost of ownership. A platform with slightly higher fees might justify them with superior performance or advanced features.

Investors should evaluate these factors based on their individual financial goals, risk tolerance, and the level of service they require, ensuring a comprehensive understanding of Robo-Advisors Performance Fees.

Performance Highlights Across Platforms

- Vanguard Digital Advisor: Known for consistent, market-tracking performance due to its index-based ETFs.

- Betterment: Often cited for strong after-tax returns due to effective tax-loss harvesting.

- Wealthfront: Delivers competitive returns, with an emphasis on advanced tax optimization and diversified portfolios.

- Schwab Intelligent Portfolios: Solid performance for a no-advisory-fee model, though cash drag can be a factor.

- Fidelity Go: Reliable performance backed by Fidelity’s investment management expertise.

Fee Structure Comparison

Advisory fees for the top platforms typically range from 0.00% to 0.35% of AUM, while underlying ETF expense ratios are usually between 0.05% and 0.15%. Schwab Intelligent Portfolios offers 0% advisory fees, but includes a cash allocation.

Betterment and Wealthfront generally charge 0.25% of AUM for their basic service tiers, with higher tiers offering additional features. Vanguard Digital Advisor is highly competitive, often at 0.15% of AUM.

Fidelity Go offers no advisory fee for smaller balances, making it particularly attractive for new investors. These varied structures highlight the importance of detailed comparison for Robo-Advisors Performance Fees.

The Future of Automated Investing: Trends for 2026 and Beyond

The landscape of automated investing is continuously evolving, with several key trends poised to shape its future in 2026 and beyond.

Personalization is becoming increasingly sophisticated, moving beyond basic risk assessments to incorporate individual values and specific financial milestones.

Integration with broader financial ecosystems, including banking, budgeting, and lending services, is another significant development. This aims to create a more holistic financial management experience for users.

Furthermore, regulatory scrutiny and the demand for enhanced cybersecurity will drive continuous improvements in platform security and compliance, influencing how Robo-Advisors Performance Fees are structured and communicated.

Enhanced Personalization and AI Integration

- Hyper-Personalized Portfolios: AI will allow for even more granular customization, incorporating environmental, social, and governance (ESG) preferences and unique life events into portfolio construction.

- Predictive Analytics: Advanced AI will offer more precise financial forecasting and proactive advice, anticipating user needs and market changes.

- Behavioral Finance Integration: Platforms will increasingly use insights from behavioral economics to help users make better financial decisions, mitigating common biases.

Expanding Service Offerings

Robo-advisors are moving beyond just investment management to offer a wider array of financial services. This includes automated savings tools, debt management advice, and even access to human financial planners for complex situations.

The goal is to become a comprehensive financial hub for users, simplifying their financial lives and providing a single point of access for various needs. This expansion adds value beyond traditional investment returns.

Such comprehensive offerings will likely influence the perception and value derived from Robo-Advisors Performance Fees, potentially justifying higher costs for integrated services.

Choosing the Right Robo-Advisor for Your Needs

Selecting the ideal robo-advisor involves more than just looking at raw performance numbers and advertised fees. It requires a thorough understanding of your personal financial situation, investment goals, and risk tolerance.

Consider the level of human interaction you might desire; some platforms offer access to certified financial planners, while others are purely automated.

Assess the platform’s features, such as tax-loss harvesting, goal tracking, and integration with other financial tools.

Ultimately, the best robo-advisor is one that aligns with your specific needs, provides transparent communication, and offers a clear path to achieving your financial aspirations, all while maintaining a competitive Robo-Advisors Performance Fees structure.

| Key Aspect | Brief Description |

|---|---|

| Performance Metrics | Focus on risk-adjusted returns, diversification, and market resilience. |

| Fee Structures | Compare advisory fees, expense ratios, and total cost of ownership carefully. |

| Top Platforms | Vanguard, Betterment, Wealthfront, Schwab, Fidelity offer diverse options. |

| Future Trends | Enhanced personalization, AI integration, and expanded service offerings. |

Frequently Asked Questions About Robo-Advisors

A robo-advisor is an automated digital platform that provides algorithm-driven financial planning services with little to no human supervision. It works by collecting information about your financial situation and risk tolerance, then constructs and manages a diversified portfolio of ETFs or mutual funds for you, often including automated rebalancing and tax-loss harvesting.

Robo-advisors are particularly well-suited for investors who are comfortable with digital platforms, seek low-cost investment management, and prefer a hands-off approach. While they cater to a wide range of investors, those with complex financial situations or a strong preference for human interaction might find traditional advisors more appropriate.

Robo-advisors generally charge significantly lower fees, typically ranging from 0.15% to 0.50% of assets under management (AUM) annually, plus underlying fund expense ratios. Traditional financial advisors often charge 1% or more of AUM, making robo-advisors a more cost-effective option for many investors seeking insights into Robo-Advisors Performance Fees.

The primary benefits include lower costs, accessibility (low minimums), automated portfolio management, diversification, and often sophisticated features like tax-loss harvesting. They simplify investing, making it easier for individuals to build and maintain a diversified portfolio without extensive financial knowledge, directly impacting Robo-Advisors Performance Fees considerations.

When choosing a robo-advisor, consider its fee structure, investment methodology, available features (e.g., tax-loss harvesting, human advisor access), minimum investment requirements, and your personal financial goals and risk tolerance. Researching Robo-Advisors Performance Fees and understanding how they align with your needs is crucial for making an informed decision.

Looking Ahead: The Evolving Landscape of Robo-Advisors

The ongoing evolution of The Rise of Robo-Advisors: Comparing Performance and Fees for 5 Top Platforms in 2026 suggests a future where automated financial guidance becomes even more integrated into daily life.

Investors should anticipate continued innovation in personalized service, ethical investment options, and seamless integration with broader financial tools.

Understanding the rise of the robo-advisor and how fintech is disrupting retirement can offer valuable perspective on these structural changes.

Staying informed about these developments will be key to leveraging the full potential of these platforms for long-term financial success.

The dynamic interplay between Robo-Advisors Performance Fees and evolving technology will continue to shape investor choices.